The best and worst countries in Latin America and the Caribbean this year.

BY JOHN PRICE

Homegrown political transformation, record metals prices, the energy sector, and yes, Donald Trump, are all playing a role in shaping the economic opportunities to be found in Latin America this year.

Compared to the last time we evaluated LatAm markets (2024) using our proprietary index, the most improved performer is clearly Argentina. Javier Milei, who many international observers wrote off as a quack while campaigning for president, has been able to execute—and now started to legislate—a bold, libertarian agenda that promises not only to upend Argentina’s moribund economy, historically riddled with corrupt government, belligerent unions, over-regulation and investor malaise, but also provides a blueprint for the emerging roster of center-right presidencies to implement.

Cartel violence in Mexico, a humanitarian crisis in Cuba, and uncertainty in Venezuela may dominate the headlines, but there is a tectonic shift underway in Latin America that, through political change, promises economic policies that are more pragmatic, less regulated and possibly less taxed in the future. Across Latin America as a whole, 2026 promises less capital flight, more investment, strong LatAm FX, and higher trade volumes.

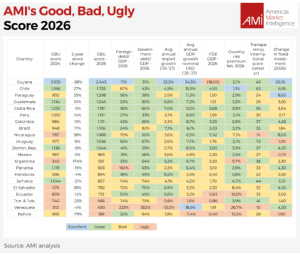

But disparities between Latin American markets remain, hence the need for AMI to shed light objectively on those differences and alert investors and exporters as to where genuine opportunities and risks exist in 2026. These are the reasons we publish each year our Good, Bad and Ugly analysis of the region.

THE GREAT

Guyana

Guyana’s 2026 story is no longer “oil is coming.” It’s “oil is here—and the real constraint is national execution.” The country’s fiscal stance is being set explicitly to convert oil-linked inflows into visible, non-oil capacity: roads, housing, health, and public administration. In the official 2026 Budget Speech (Ministry of Finance), the government frames the year as a scaling moment for delivery systems, not just spending lines.

The political center of gravity remains President Irfaan Ali and the governing PPP/C’s commitment to a “build-out” agenda. In domestic coverage around the budget, Ali has swatted back criticism that Guyana’s performance is superficial or purely state-driven, calling that critique “comical.” And yet, private FDI this year will be negative as massive investment bets made over the last six years now generate enormous profit repatriation.

Guyana’s oil trajectory anchors U.S. strategic attention: China’s presence is material through the upstream consortium (CNOOC stake) and broader contracting, but the dominant geopolitical fact is that U.S. policy covets stability around this new Atlantic oil basin. Exxon’s multi-project development pipeline is the country’s economic metronome: Yellowtail started in 2025 (250k bpd) and Uaru is expected to start in 2026, expanding capacity and enabling downstream gas/power industrialization ambitions.

What’s investable in 2026 for Guyana: Construction supply chains, engineering services, industrial inputs, logistics, telecom upgrades, and anything that solves productivity bottlenecks (ports, warehousing, power, skilled labor). Investors with operational discipline can win because procurement and project management are becoming the edge—not “finding demand.”

Key 2026 investment risks for Guyana: The classic “too much, too fast” set: inflation in rents/wages, governance stress, and Dutch-disease temptations. Still, in 2026, Guyana is the region’s clearest “capacity build” super cycle—and still Great, even if you underwrite execution risk honestly.

We invented the Great classification to accommodate Guyana’s off-the-charts score in our Good, Bad, Ugly (GBU) index. But it is worth noting the Guyana’s score fell 38% from 2024 and may fall further to earth as its growth projections slow from electrifying to fast.

THE GOOD

Chile

José Antonio Kast won the December 2025 runoff election and is due to take office on 11 March 2026. That transition matters because investors don’t price “left vs. right” in Chile so much as predictability, permitting speed, and security outcomes. Kast’s mandate is built on a promise to restore order and unlock growth, but he inherits a congress without an automatic majority—meaning policy ambition must confront legislative arithmetic.

The Banco Central de Chile has been signaling a 2026 growth band closer to “steady recovery” than boom, and—critically for investors—Chile’s policy transparency remains a comparative advantage (clear communications, scheduled reporting, and a credible inflation framework). Moderate real growth will none-the-less translate into impressive nominal USD GDP growth thanks to Chilean peso that is destined to appreciate on the back of rising metal prices, returning capital and investor confidence.

Despite the political pivot to the right, Chile will strive to keep relations positive with both the US and China. Chile is structurally close to the U.S. in capital markets and mining services, but China is the dominant marginal buyer for minerals and a key stakeholder via lithium and mining supply chains.

What’s investable in 2026 for Chile: Anything tied to long-cycle competitiveness—mining services, grid upgrades, water and desalination, permitting tech, and supply chain localization around copper/lithium. If Kast meaningfully reduces permitting friction and improves security conditions, you could see capex pipelines move from “intended” to “executed.”

Key 2026 investment risks for Chile: Social pushback if fiscal tightening or security measures feel heavy-handed; and project delays if coalition-building fails.

Chile is Good because institutions still anchor the cycle—even in a political reset. Chile’s score has improved 27% since 2024 thanks to a more promising political/investment climate ahead and very favorable metal price trends.

Paraguay

Paraguay is the region’s quiet outperformer in 2026, rising 35% on its GBU score since 2024, because it offers something scarce: high growth with macro and policy predictability. The Banco Central del Paraguay (BCP) projects real GDP growth of 6.0% in 2025 and 4.2% in 2026, with inflation converging gradually toward the 3.5% target in 2026.

Paraguay’s business climate advantage is institutional continuity and the credibility dividend from achieving broader market access. Its “political risk” is less electoral shock and more whether discipline holds (fiscal, anti-corruption, institution-building).

Paraguay is strategically pivotal because it remains a Taiwan-recognizer, making it a target of PRC diplomatic pressure and a point of U.S. interest in regional alignment. President Santiago Peña has rather effectively cozied up to US President Trump and Secretary of State Rubio.

What’s investable in 2026 for Paraguay: Agribusiness value chains, services and commerce tied to strong household demand, and manufacturing/logistics that benefit from the country’s “boring but functional” operating environment. The upside is amplified by Paraguay’s improved external reputation—especially following its investment-grade upgrade (by two of the three major ratings agencies) which lowers the cost of capital and broadens the investor base.

Key 2026 investment risks for Paraguay: Mostly exogenous rather than self-inflicted: drought/climate effects on agriculture, commodity cycles, and spillovers from neighbors.

Guatemala

Guatemala’s 2026 economic status is a classic “macro stability, micro constraints” story. Domestic commentary for 2026 repeatedly points to an official growth figure of around 4.1%, supported by remittances, household demand, and services exports. This is the “good news.” The “Guatemala constraint” remains institutional friction: project permitting, security costs, and uneven rule enforcement.

The political variable with the biggest commercial consequence remains whether the government can improve governance capacity without triggering elite pushback or legal instability. President Arevalo’s deft rapprochement with Washington helps keep his right-wing domestic opponents at bay.

What’s investable in 2026 for Guatemala: Agribusiness value chains, light manufacturing (where logistics can be controlled), BPO and services in stronger urban nodes, and “infrastructure-adjacent” services rather than mega-projects.

Key 2026 investment risks for Guatemala: Security, governance disputes, and execution bottlenecks that add time and cost.

Net: Good in 2026, 10% above its 2024 GBU score, because the macro floor looks firm, but strategic investment returns depend heavily on local operating capability.

Costa Rica

The business climate is being reset by the decisive election of Laura Fernández, who won the presidency in the first round (c. 48% of votes) and her Sovereign People’s Party is projected to hold an unusually strong legislative position (a rarity since 1990). That reduces “gridlock risk,” but raises a different risk: how far the new government tests institutional limits in the name of security and constitutional change.

Fernández has framed her win as the beginning of a new political era—Reuters reports her declaring the start of a “third republic.” (an ominous sounding title to any with an ear for history). Investor sentiment in 2026 will follow two variables: (1) whether public security actions reduce crime without eroding rule-of-law, and (2) whether the pro-business narrative is matched by clean, predictable execution.

On the economy, the Banco Central de Costa Rica projects moderation after a strong 2025: “En el 2026 el crecimiento sería moderado (3,8%),” according to its January 2026 Monetary Policy Report. This is still a strong figure relative to the region. Nearshoring services, medical devices, and high-value exports remain the structural drivers, even if certain, mostly lower-value, FDI projects rotate out.

What’s investable in 2026 for Costa Rica: Export services, industrial/medical supply chains, and selective infrastructure that reduces logistics costs.

Key 2026 investment risks for Costa Rica: Institutional temperature and the security model.

Net: Good—with a rule-of-law “watchlist” embedded in the evaluation. The added political risk has brought down Costa Rica’s GBU score slightly by 5% since 2024.

Peru

Peru is the region’s clearest example of “politics as a recurring operating cost.” José María Balcázar was recently chosen as the interim president (the 9th in 10 years), tasked with overseeing elections scheduled for April 12, 2026 (runoff expected in June). This political instability raises the hurdle rate for greenfield projects and pushes investors toward brownfield/shorter-cycle bets.

Despite the political turmoil that has spanned a decade, Peru’s currency is the most stable in the region, thanks to several economic anchors: an over-sized mining sector that generates massive dollar income (especially now with record gold and copper prices), arguably the hemisphere’s best managed central bank, led by Julio Velarde (BCRP governor), a Fujimori shrunken government, and correspondingly limited tax burdens.

Peru’s problem is rarely macro capability; it’s governance continuity. Mining and infrastructure remain world-class opportunities, but investors price in delays: permitting, community conflict, and shifting political signals. In 2026, the election environment amplifies those risks, because candidates often campaign against “extractivism” even when budgets depend on it.

What’s investable in 2026 for Peru: Treat Peru as a “pipeline management” year—advance permitting, local partnerships, and risk mapping—rather than assuming rapid greenlights. Sectors with near-term resilience include consumer staples, logistics, and mining services that are less exposed to greenfield political battles.

Key 2026 investment risks for Peru: Every national election in Peru is a risk wild card. Political parties have lost strength such that Presidential politics is a battle of personalities (more than 30 candidates at last count for the April 2026 election), leading to outlandish promises and campaign platforms. There is no clear path to political stability in Peru where a President can fulfill his or her mandate for the full five-year period. Peru’s economic stability relies on long term adherence to its mining code and sage management of an independent central bank. Any threat to these two institutional pillars and Peru’s autopilot economy goes off the rails.

Despite the political noise, Peru’s economic growth prospects are strong in the short-term. As a result, Peru has climbed 14% in our GBU index since 2024.

Colombia

2026 is election-saturated: Congress elections (March 8) and the subsequent presidential cycle turn policymaking into campaign signaling. Even if institutions function, uncertainty delays long-cycle capex—especially in energy and regulated sectors.

With President Gustavo Petro shaping the narrative and opposition attempting a reset, the market’s baseline in 2026 is “wait and price.” Investors delay irreversible bets, especially in energy and long-cycle infrastructure, until post-election clarity emerges.

Under Petro, Colombia deepened its China engagement, including a Belt & Road cooperation plan—moves that raise U.S. concern and increase scrutiny for sensitive sectors (telecom, infrastructure, ports).

Colombia still has structural strengths: scale, diversified industry, and a sophisticated corporate ecosystem. But in 2026, risk premia are driven by (1) security trends in certain corridors, (2) regulatory signals around energy, and (3) fiscal flexibility.

What’s investable in 2026 in Colombia: Sectors with embedded demand and lower regulatory discretion—select consumer, tech-enabled services, logistics, and projects that can be phased. Foreign strategic investors can win by structuring step-in rights and political-risk mitigants; financial investors win by avoiding “headline-sensitive” assets that trade on every poll.

Key 2026 investment risks for Colombia: Colombia can ill afford another four years of lame duck politics, where the nation’s institutions strain to contain the destructive instincts of another populist President. It is unlikely that a politically centrist candidate will make it to the run-off election on June 21st, 2026, so a populist is likely to win. The markets will let us know which they prefer, a populist on the left or the right. Neither prospect is ideal.

Colombia has climbed 13% in its GBU score since 2024 thanks to favorable commodity prices, a lame-duck Presidency, hemmed in by strong institutions and the prospect of more sensible political leadership in the near future.

Brazil

2026 is a year of election gravity. Markets price the risk of fiscal loosening and policy noise, even if institutions are strong. Monetary policy is the second headline. The Banco Central do Brasil (Copom) held the Selic at 15.00% in its January 2026 meeting, and its official communications emphasize that inflation expectations for 2026 remain above target, and the external environment remains uncertain. Recent Reuters reporting indicates the central bank is signaling the start of a rate-cut cycle—while insisting policy will stay restrictive until inflation is anchored.

For investors, that’s the 2026 posture: easing may come, but Brazil is not returning to cheap money quickly. That restrains some domestic-demand sectors but supports disinflation credibility. It also keeps the Real strong and with it import growth.

The recent SCOTUS decision to strike down President Trump’s IEEPA tariffs (based upon a perceived national emergency) will bring some relief to Brazil’s trade balance and boost the Real even further.

What’s investable in 2026 for Brazil: Energy, infrastructure, export sectors, and businesses that can thrive even under higher-for-longer interest rates.

Key 2026 investment risks for Brazil: Fiscal drift, noisy politics, and global risk-off episodes that hit Brazil’s FX and rates.

Brazilian growth has proven resilient and the highest real interest rates in the world provide for strong import appetite, a boon for global exporters. Centrist congressional politics keep populism at bay. As a result, Brazil has climbed 17% in our GBU scoring since 2024.

Nicaragua

Nicaragua seems oddly placed as a “Good” country in our annual evaluation, but numbers do not lie, even if investor risk is real. The Banco Central de Nicaragua projects 2026 growth in a 3.5%–4.5% range and low unemployment. Foreign direct investment continues to grow thanks to the Ortega’s preferential treatment of the mining sector, which is buoyed by record high gold and silver prices. The government’s rapid approvals of mining permits and heavy-handed treatment of local mining opponents and unions has made Nicaragua an attractive place to operate for mining juniors. Mining majors stay away because of the reputational risk of getting too close to an abusive political autocrat.

For the moment, Nicaragua has escaped the ideological wrath of US Secretary of State Marco Rubio who is busy trying to transform Venezuela and Cuba. Eventually, Nicaragua’s political pariah status will hurt its economic well-being, but that moment may not arrive in 2026 as record metal prices and continued remittance flows enrich consumers and boost imports. As a result, Nicaragua climbed 38% in its GBU score versus 2024.

What’s investable in 2026 for Nicaragua: Typically, those that can (a) operate with limited legal exposure, (b) generate hard currency, and (c) structure repatriation and governance protections.

Key 2026 investment risks for Nicaragua: External pressure, sanctions dynamics, and domestic political tightening.

Uruguay

Uruguay remains the region’s premium “low drama” market in 2026: stable institutions, predictable rule-of-law, and a central bank that communicates like a grown-up. The Banco Central del Uruguay notes that GDP growth projections were “stable for 2026”, even as other years see mild revisions. That’s exactly what investors pay for: fewer surprises. Improving export prospects in Argentina and Brazil help raise Uruguay’s GBU score by 8% vis-à-vis 2024.

What’s investable in 2026 for Uruguay: The key 2026 business climate driver is not electoral shock but maintaining competitiveness (tax, regulation, labor) while neighboring volatility creates spillovers. That makes it attractive for regional holding structures, services exports, renewables-adjacent investment, and regulated-sector plays that require legal consistency.

Uruguay’s foreign posture tends to be pragmatic: U.S. for finance and investment standards; China for commodities and market access. The 2026 commercial question is whether Uruguay can widen export opportunities while keeping its “rules-based” brand intact.

Key 2026 investment risks are mostly external: Argentina/Brazil cycles, commodity prices, and global rates. Internal risks are about scale—Uruguay can’t absorb unlimited capital quickly without compressing returns.

Dominican Republic

The Dominican Republic remains the Caribbean’s “big, small market” that investors can underwrite with fewer heroic assumptions. The Banco Central de la República Dominicana has laid out a clear 2026 baseline: growth “en torno a 4.0% para 2026,” supported by public and private investment and resilient services. That’s the right kind of growth: not a one-off sugar high, but a continuation of a broad services/tourism platform with manufacturing and logistics upside.

The political calendar is part of the appeal: 2026 is not a presidential cliff year, so the question is execution—airport/port capacity, electricity reliability, and workforce skills—rather than sudden regime change. For strategic investors, macro stability has always been the country’s appeal while project execution challenges (red tape, corruption, labor productivity & quality, and infrastructure bottlenecks) have handicapped returns. Changing those structural weaknesses has been a focus of the Abinader government but such transformation requires a generation, not a half decade. That reality takes some of the sheen off of the GBU score for the DR, which declined 8% since 2024.

The DR’s U.S. relationship (tourism flows, remittances, trade and finance) is the central macro stabilizer. China has a growing diplomatic/economic profile, but the U.S. is still the dominant commercial center of gravity.

What’s investable in 2026 for Dominican Republic: Hospitality expansion, logistics/warehousing, industrial parks, payments/fintech for tourism and retail, and healthcare services.

Key 2026 investment risks for Dominican Republic: U.S./Europe travel cycles, energy costs, and climate events. Haiti spillover remains a tail risk, but not (yet) an invest-ability killer for most projects.

John Price is the Managing Director of Americas Market Intelligence. With 32 years of experience in Latin American market intelligence consulting, Price has supervised nearly 1,200 client engagements and advises clients in more than 20 countries across Latin America. He can be reached at jprice@americasmi.com

This article was originally published in a new whitepaper published by the Canadian Council of the Americas, called Beyond the Build.

Republished with permission from Americas Market Intelligence.